Calculate Your Costs

Use the customize button for more accuracy

I'm Darrell, thanks for visiting my website, I'm an Independent mortgage broker and founder of Victory Mortgage with our office located at

446 Goldstream Avenue in Colwood.

I'd love to work with you to help you get the best mortgage.

Getting the best mortgage is looking beyond just the best rate, it includes understanding different mortgage products and how they impact your long term financial goals. I bring a commitment to finding you the best mortgage despite a rapidly changing market conditions. I work with integrity, honesty and education to help coordinate your unique financial requirements to the best product to save you money and time.

In my spare time I enjoy time with my family. I have a passion for aviation history and history in general. Friends and family are very important to me and I enjoy sharing as much time as I can with them in this beautiful city.

I understand mortgage financing deeply and invite you to use my expertise and experience to your advantage. Let's get together and talk a bit so I can really get to know your situation and provide tailored mortgage advice.

Nice things people have said about working with me.

Finding the best mortgage can be frustrating. It doesn't have to be when you follow my 3 step plan.

Get started right away

The best place to start is to connect with me directly. My commitment is to listen to your needs, assess your financial situation, provide professional mortgage advice, and

guide you through the mortgage process.

Get clarity

Sorting through all the different mortgage lenders, rates, terms, and features can be overwhelming.

Let me cut through the noise. I'll outline the best mortgage products available with your needs in mind.

Proceed with confidence

My goal is to make sure you know exactly where you stand at all times. From your initial application through your mortgage renewal, I'm available to answer any questions for as long as you need a mortgage.

I've got you covered.

Get started by completing my online mortgage application.

I'll let you know exactly where you stand so you can proceed with confidence.

Go ahead and book a call with me.

Let's run some numbers

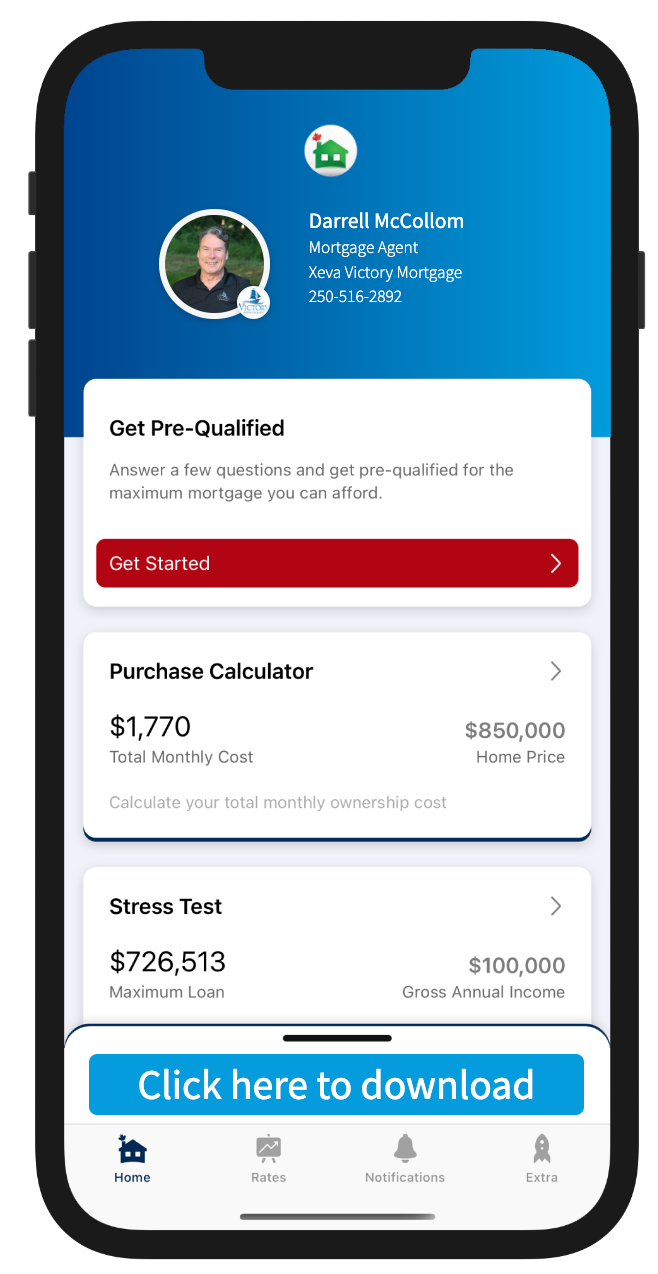

Download my app

What you can do with my app

Calculate your total cost of owning a home

Estimate the minimum down payment you need

Calculate Land transfer taxes and the available rebates

Calculate the maximum loan you can borrow

Stress test your mortgage

Estimate your Closing costs

Compare your options side by side

Search for the best mortgage rates

Email Summary reports (PDF)

Use my app in English, French, Spanish, Hindi, and Chinese

Everything you need,

all in one place

As a trusted mortgage provider, let me help you with these services.

Click through any of the services to learn more

Mortgage articles to keep you informed.